" Historical S&P500 Price to Earnings Ratio Chart "

Return to KirkLindstrom.com home page

|

S&P500 PE & CAPE History " Historical S&P500 Price to Earnings Ratio Chart " |

|

Return to KirkLindstrom.com home page |

|

|

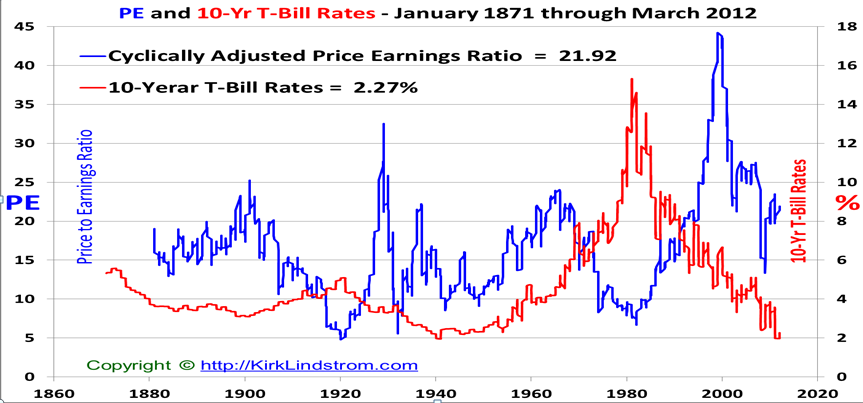

| March 30, 2012: PE

ratios usually fall when investors slowly lose interest in

stocks. The exceptions are bear market crashes when

companies lose money and write off everything but the

kitchen sink to often show negative earnings. Table and excerpt from my April 2012 Newsletter:

P/E10, or CAPE

(Cyclically Adjusted Price Earnings) Ratio

In 1984, shortly after CAPE bottomed around 7, I bought my first home using a 14.0% variable rate loan. Fixed loans were about 17% at that time. A few months ago, I refinanced my home mortgage with a fixed 3.375% 15-year loan. |

||

|

The S&P500 came very

close to having zero earnings at the peak of the

financial crisis. When you divide

stock price by nearly zero earnings, you get a

very, very high PE.

From Chartoftheday.com1 Today's chart illustrates how the recent rise in earnings as well as recent stock market action has impacted the current valuation of the stock market as measured by the price to earnings ratio (PE ratio). Generally speaking, when the PE ratio is high, stocks are considered to be expensive. When the PE ratio is low, stocks are considered to be inexpensive. From 1900 into the mid-1990s, the PE ratio tended to peak in the low to mid-20s (red line) and trough somewhere around seven (green line). The price investors were willing to pay for a dollar of earnings increased during the dot-com boom (late 1990s), surged even higher during the dot-com bust (early 2000s), and spiked to extraordinary levels during the financial crisis (late 2000s). As a result of the continued surge in corporate earnings the PE ratio remains at a level not often seen since 1990 despite what has been a significant upward trend in stock prices so far this calendar year.

Article:

Beware

of

Annuities

|

|

|

|

Note 1. Source:

Chart of the

Day "Journalists and bloggers

may post the above free Chart of the Day on their

website as long as the chart is unedited and full

credit is given with a live link to Chart of the Day

at http://www.chartoftheday.com."

|

||

|

||

| KirkLindstrom.com Home of "CORE & Explore®" investing. |

Blog |

|||

FREE=> Investment

Letter

SAMPLE <==

FREE

Disclaimer: The information contained in this seb site is not intended to constitute financial advice, and is not a recommendation or solicitation to buy, sell or hold any security. This blog is strictly informational and educational and is not to be construed as any kind of financial advice, investment advice or legal advice. Copyright © 2012 Kirk Lindstrom. Note: "CORE & Explore®" was coined by and is a registered trademark of Charles Schwab & Co., Inc. |

||||