Implications of Bill Gross article and what it means going forward

Return to KirkLindstrom.com home page

|

|

PIMCO's Bill Gross on the Death of Equities Implications of Bill Gross article and what it means going forward |

|

| Bill Gross calls for another "death of

equities" by writing in his monthly "Investment Outlook" that "The Cult

of Equity is Dying." Return to KirkLindstrom.com home page |

|

|

||

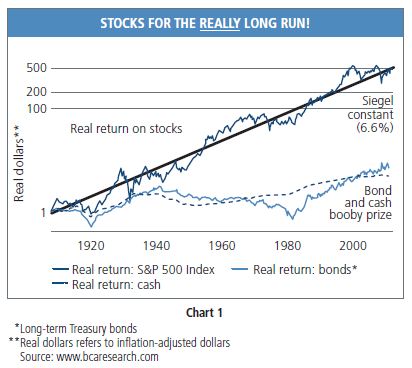

August 1, 2012: In this month's "Investment Outlook"

article, Bill Gross, the founder and co-chief investment officer of the

world's largest bond fund wrote "The cult of equity is dying." In

the article Gross explain why he thinks stocks are not really for the

long run, a play on the book by Jeremy Siegel, Stocks for the Long Run.

Note that Gross still expects equities to provide a return before

inflation going forward that is double bonds so be careful jumping to

conclusions!

In the article where Gross writes why he thinks pension funds are still too optimistic with 4.75% and higher appreciation targets, Gross gives his "new Normal" target for a diversified portfolio of 50% stocks and 50% bonds:

Implications of lower returns: What it means is all the "Monte Carlo" simulations that try to predict what a "safe withdrawal rate" is for a PASSIVE portfolio use old data that cannot be repeated going forward. It also means that all the under funded pension obligations we read about are in far worse shape than they say because the pension funds, such as CalPERS in California, are still using 7% or more for their expected total portfolio returns. (See CalSTRS Teachers Pension Fund Asset Allocation and CalPERS Asset Allocation Ratio and Target Annual Return.) On June 23, 2011, Joe Dear told CNBC the Target annual return for the CalPERS fund is 7.75%. Joe says they probably can not meet this using US equities and fixed income but he thinks they can do it if they invest globally.To get an annual return greater than zero going forward, investors will have to employ many tactics to scratch and scrape for each and every bit of extra 0.5% to 1.0% of return. These tactics include:

Of course, this is a

lot more work than having a balanced retirement portfolio that used to

allow 3% to 5% annual take-outs that many financial advisers and pension

funds still hope to get. If Gross is right, taking 5% a

year out of a portfolio that is only generating 3% a year annual return

will have you out of money sooner than you think using the old data. |

|

|

|

|

Article: Beware

of

Annuities

Article

Index

|

|

|

|

|

|

||||

| KirkLindstrom.com Home of "CORE & Explore®" investing. |

Blog |

|||

Disclaimer: The information contained in this seb site is not intended to constitute financial advice, and is not a recommendation or solicitation to buy, sell or hold any security. This blog is strictly informational and educational and is not to be construed as any kind of financial advice, investment advice or legal advice. Copyright © 2012 Kirk Lindstrom. Note: "CORE & Explore®" was coined by and is a registered trademark of Charles Schwab & Co., Inc. | ||||